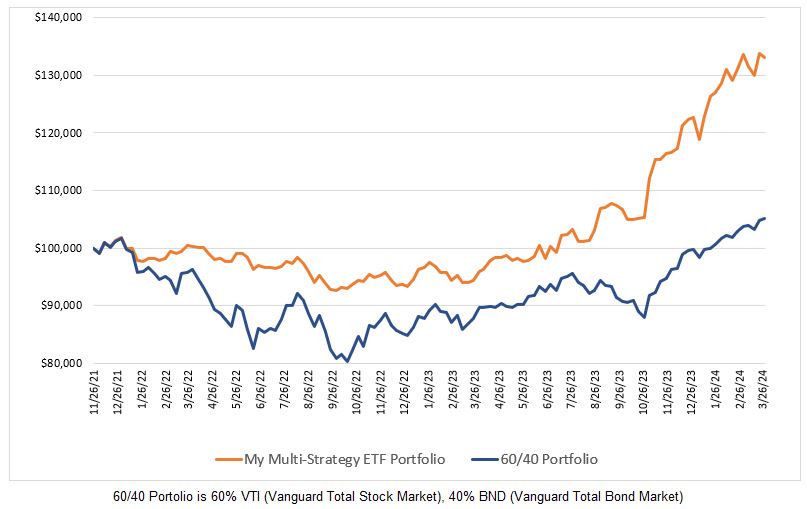

I am focusing my efforts currently on improving my trading performance through better position sizing of my trades. If you have done any research into position size optimization you will have come across the works of Ralph Vince who is one of the top experts in portfolio analysis.

Vince has written five books about money management:

Vince has written five books about money management:

- Portfolio Management Formulas: Mathematical Trading Methods for the Futures, Options and Stock Markets (1990)

- The Mathematics of Money Management: Risk Analysis Techniques for Traders (1992)

- The New Money Management: A Framework for Asset Allocation (1995)

- The Handbook of Portfolio Mathematics: Formulas For Optimal Allocation and Leverage (2007)

- The Leverage Space Trading Model: Reconciling Portfolio Management Strategies and Economic Theory (2009)

- Risk-Opportunity Analysis (2012)

In addition, he has co-authored three academic papers that are available on SSRN:

- A Dynamic Implementation of the Leverage Space Model (2012)

- Inflection Point Significance for the Investment Size (2013)

- Optimal Betting Sizes for the Game of Blackjack (2013)

If you would like to listen to Ralph Vince on a recent podcast, he has appeared with Michael Covel.

I asked Vince which of his works were most appropriate for traders like me who want to determine the optimal trading position size and he recommended the following:

- Risk-Opportunity Analysis

- Inflection Point Significance for the Investment Size

- Optimal Bet Sizes for the Game of Blackjack

Determining the optimal position size for a single system is relatively straightforward but there are a number of options to choose from and the best choice will depend on the sequence of trades which are yet to occur. In other words, the degree to which you should be aggressive or conservative in your choice of position size for the next n trades for a single system depends on an unknown – the sequence and size of wins and losses for the next n trades. Thus, there is debate over which position sizing strategy one should choose given that there are competing models and neither one is considered by most traders to be the best.

When you move from determining the optimal position size for a single strategy to determining the optimal position size for each strategy in a portfolio of strategies you will quickly discover that there is minimal published research on this topic. I asked Ralph Vince about his research in this area and he advised me that he and two others are currently working on a paper that they hope to have available on SSRN in the next three weeks.

Personally, I think that position size optimization is extraordinarily important (trade too small position sizes and your portfolio doesn’t grow near as much as it should, trade too large position sizes and you could bankrupt your account) and most traders would be well served to put more effort into this aspect of their trading.

FJP

0 Comments