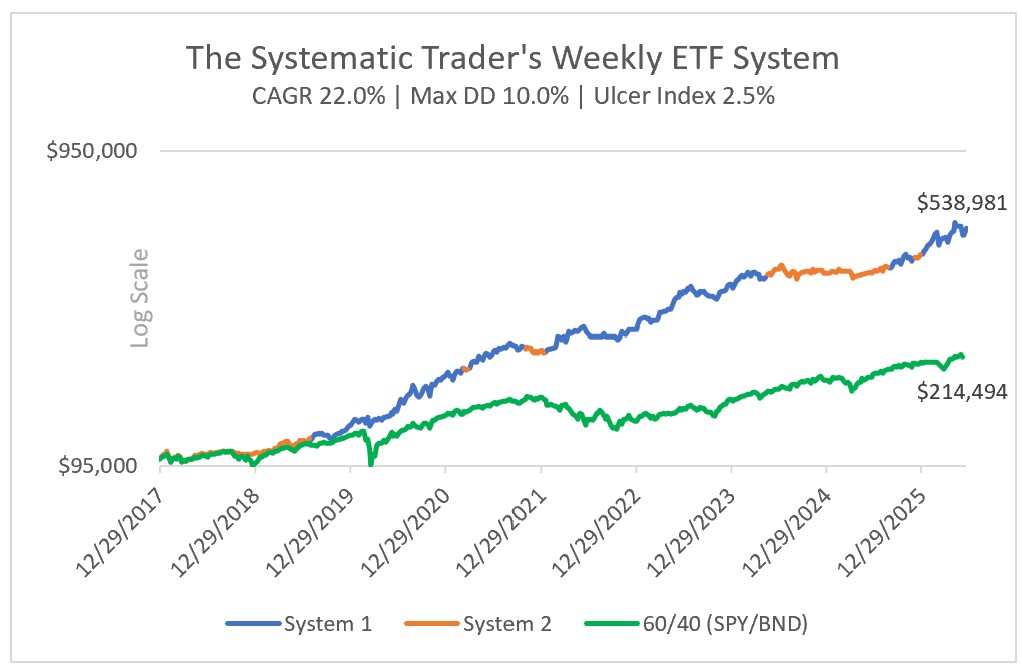

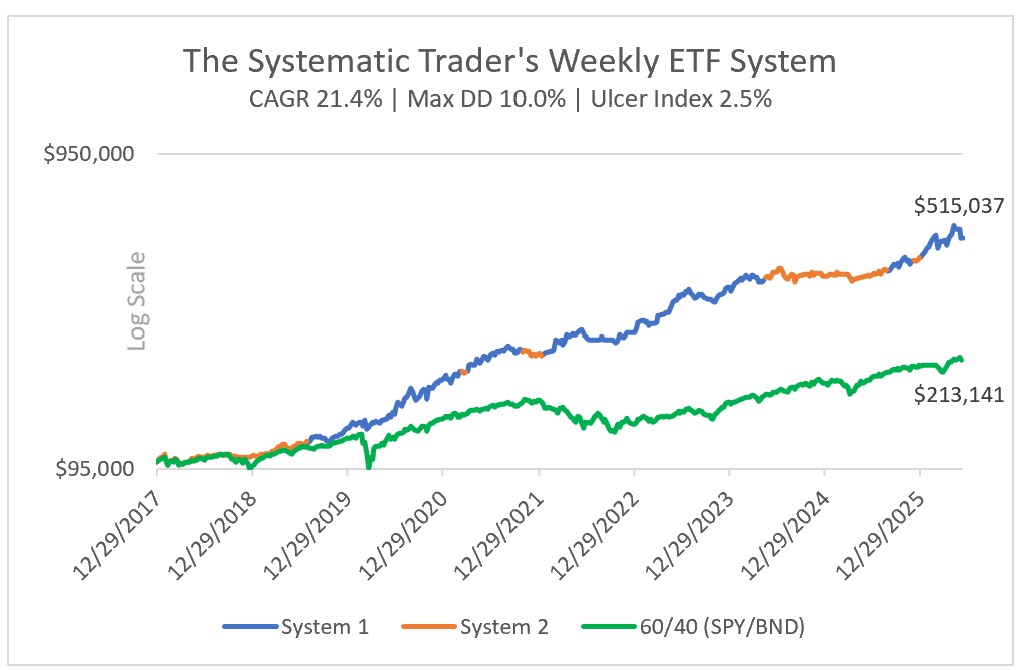

My Personal Weekly Dynamic Asset Allocations

Suggestions for ETF Allocations to Outperform the 60/40 Portfolio

Latest Posts

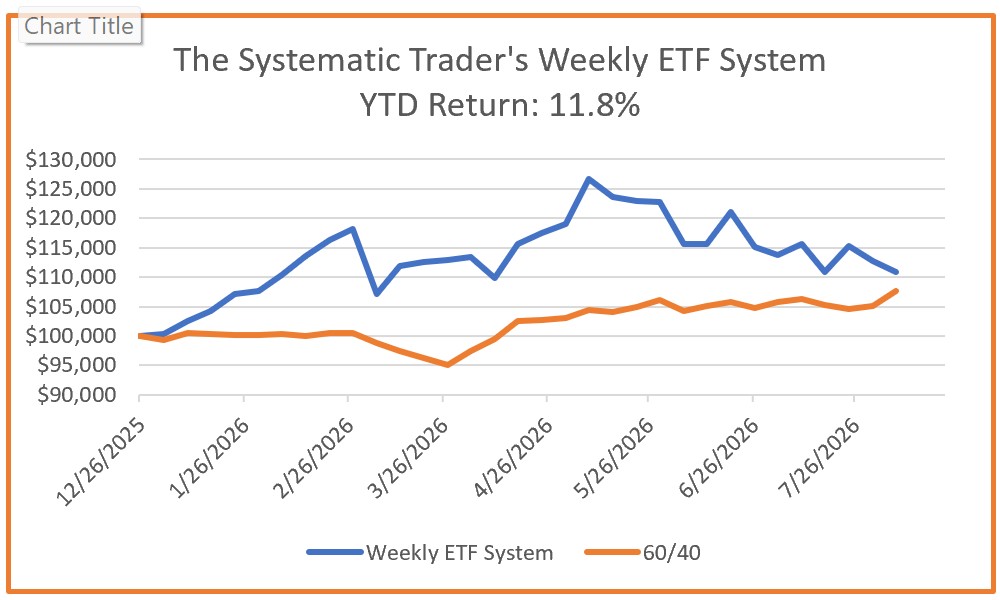

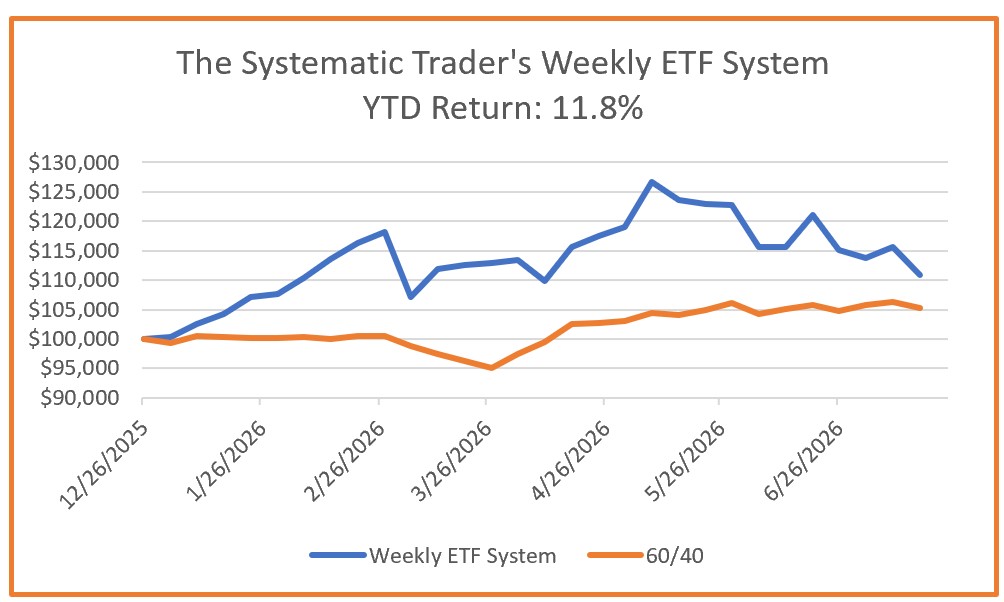

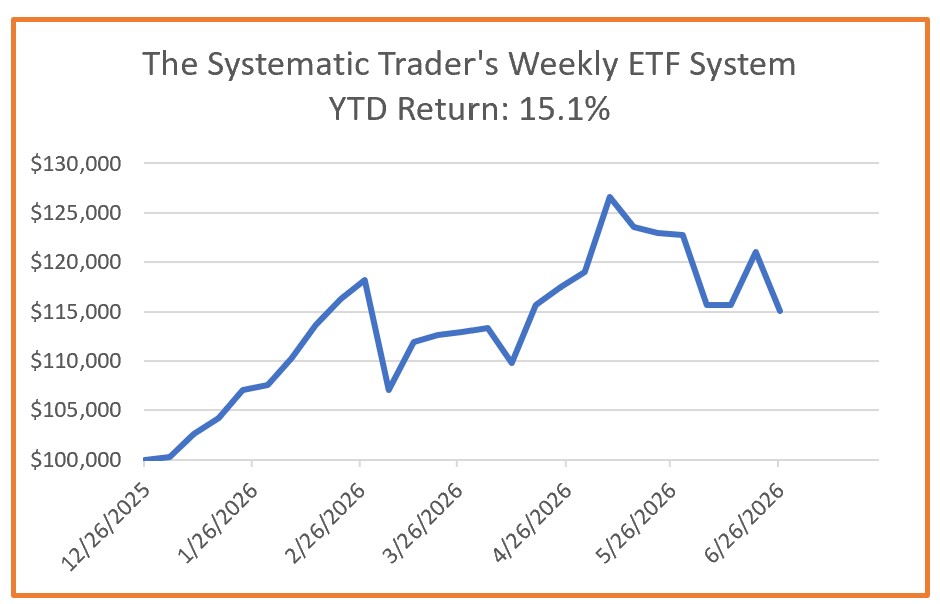

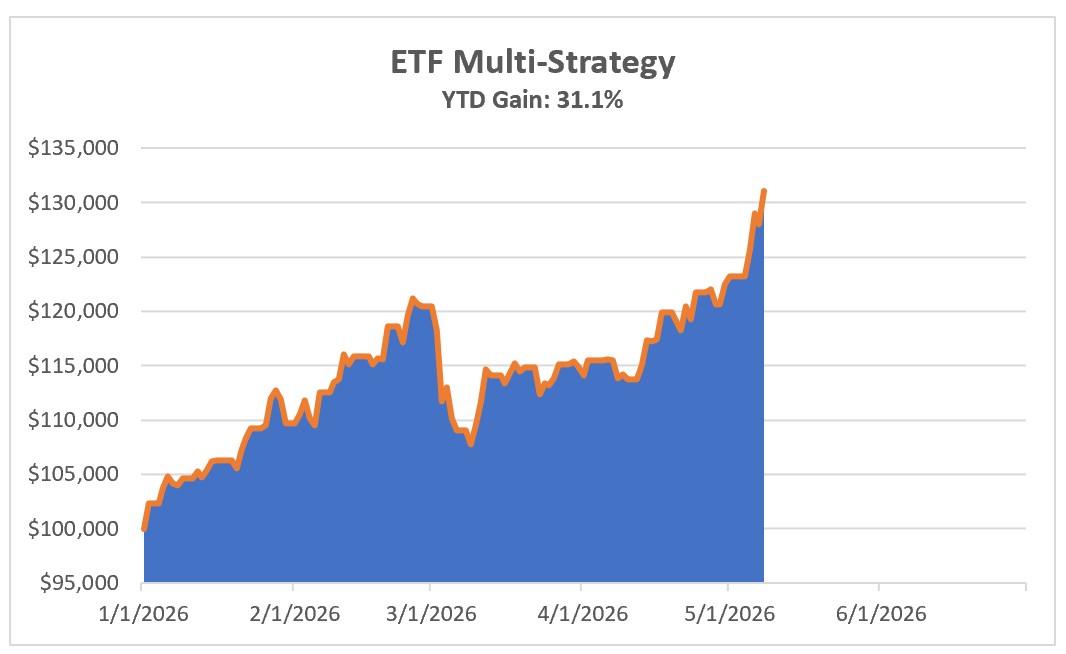

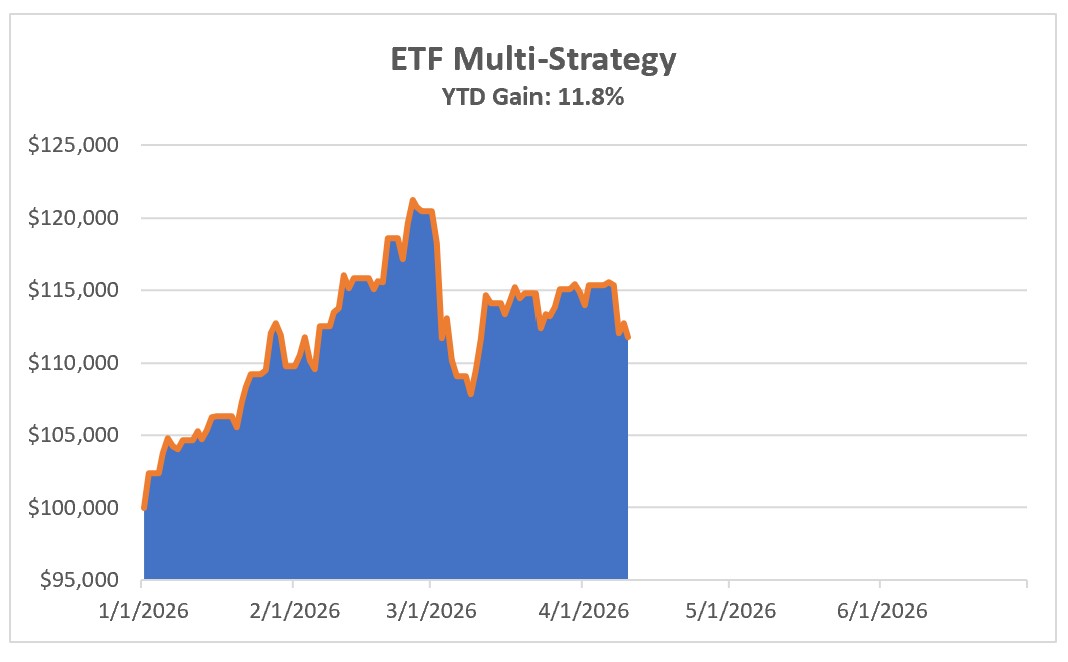

Investing Update for the Week Ending August 07, 2026

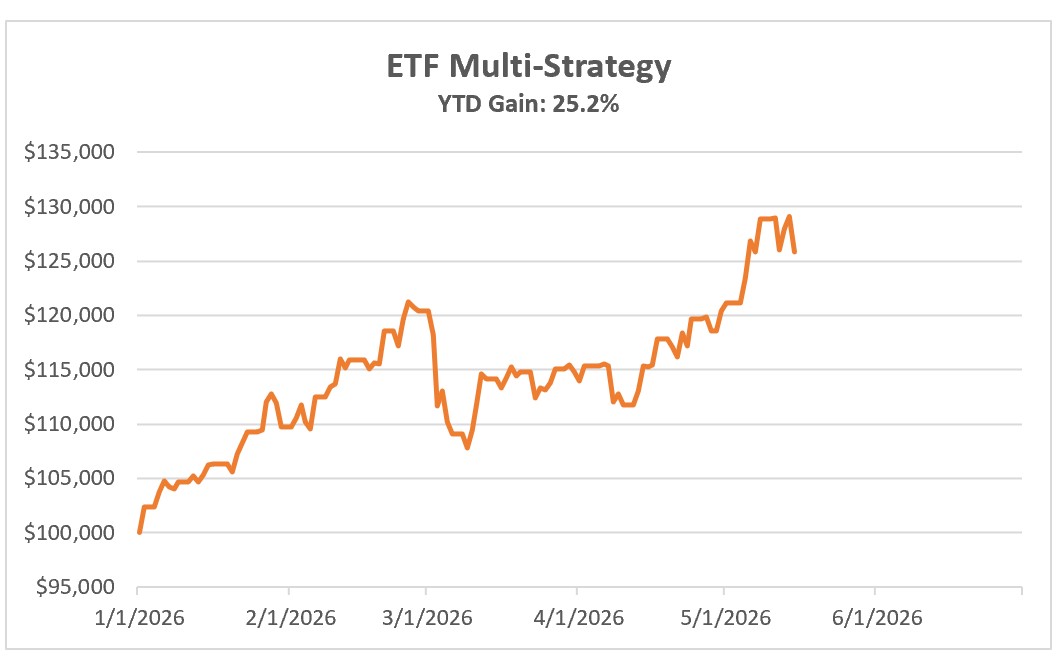

My system declined by 1.77% this week. It does remain 100% allocated to PDBC.

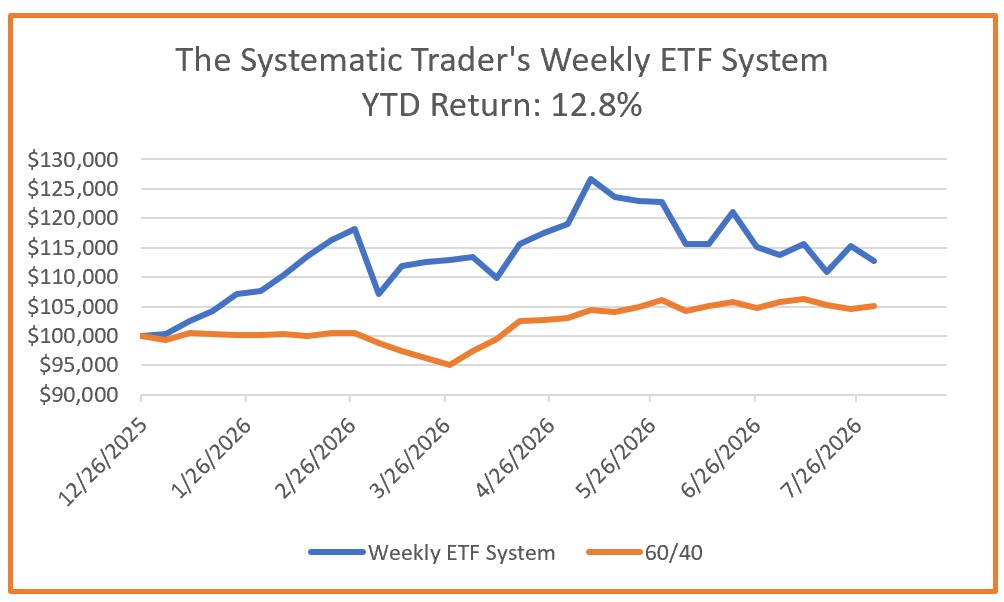

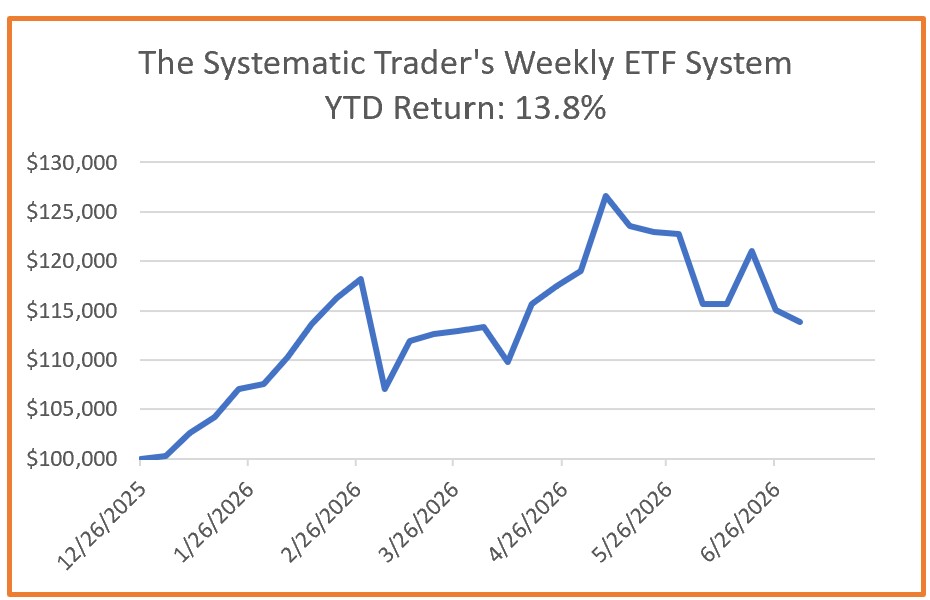

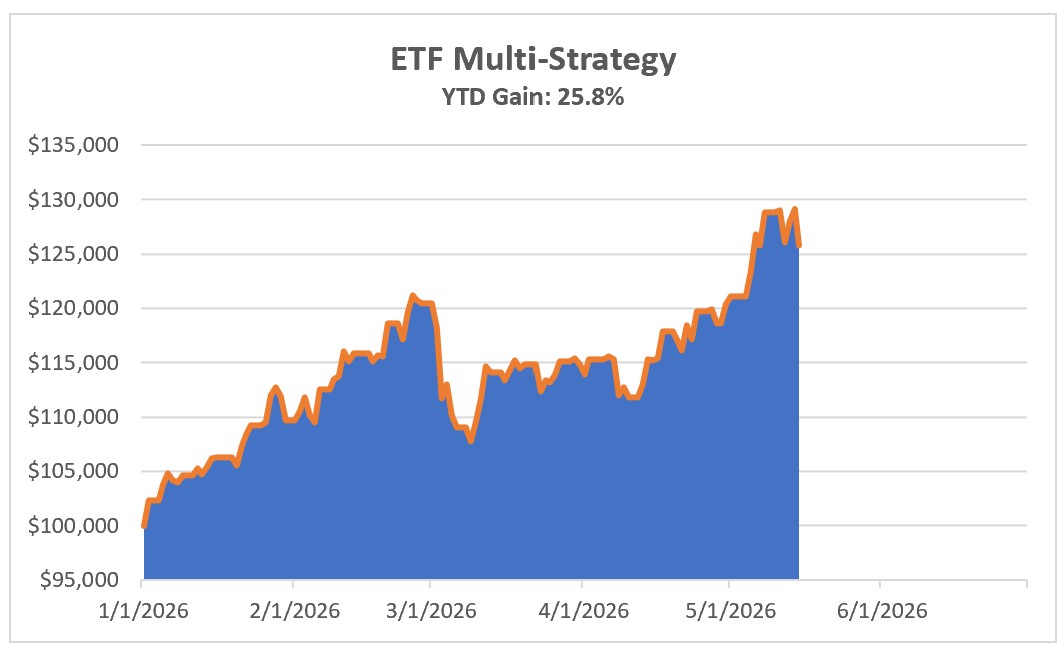

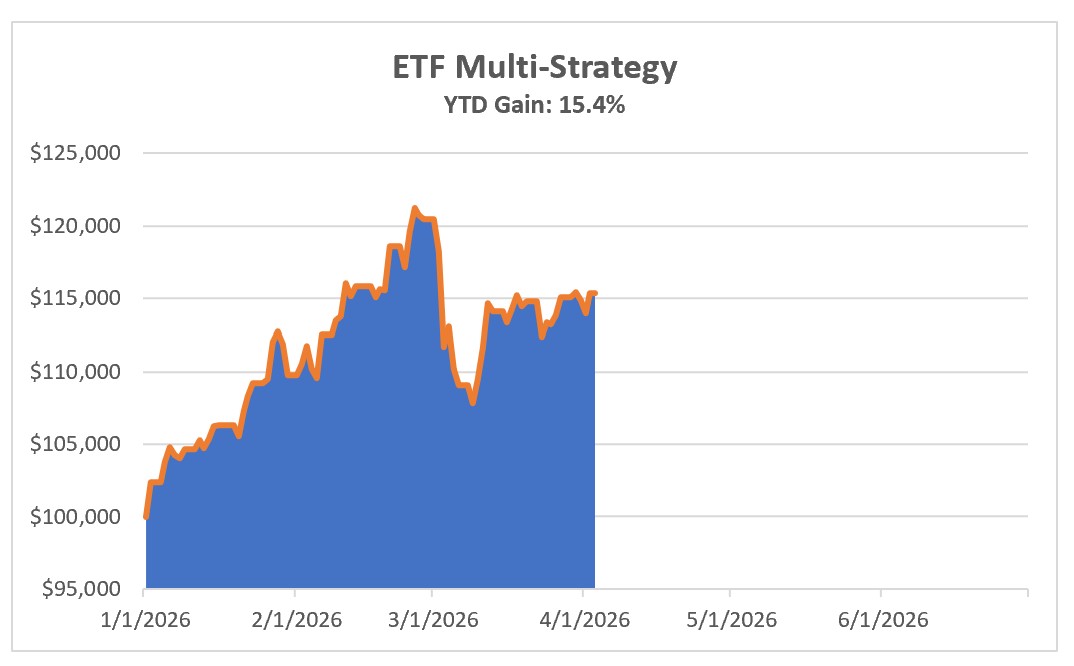

Investing Update for the Week Ending July 31, 2026

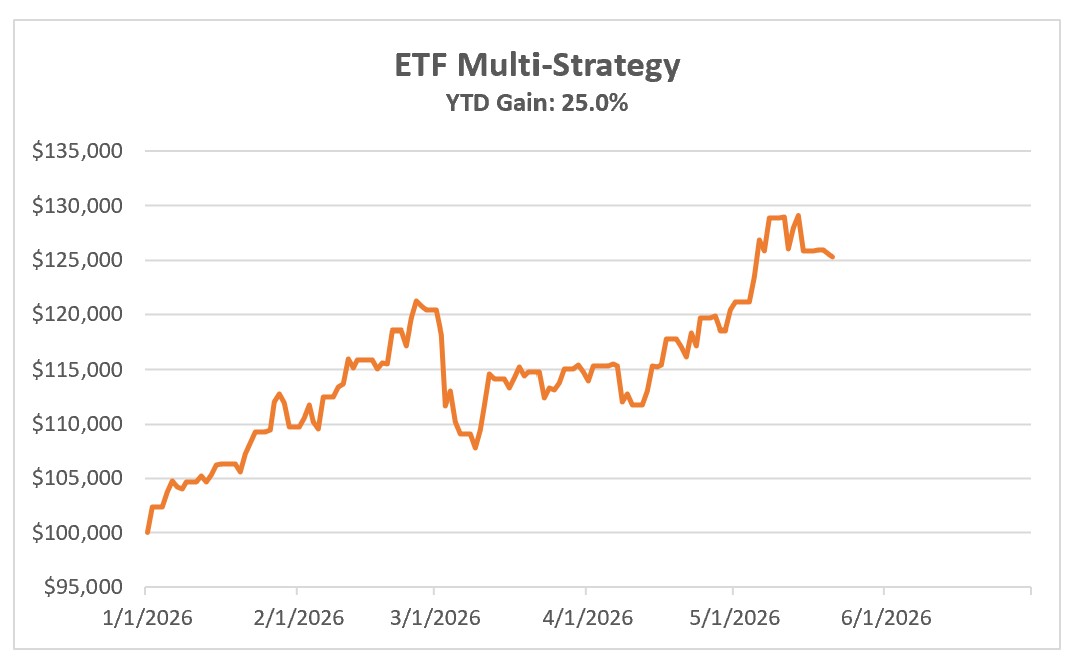

It's tough out there, folks. My ETF system fell by 2.2% this past week, but it does have a decent YTD return. There is no change in the allocation.

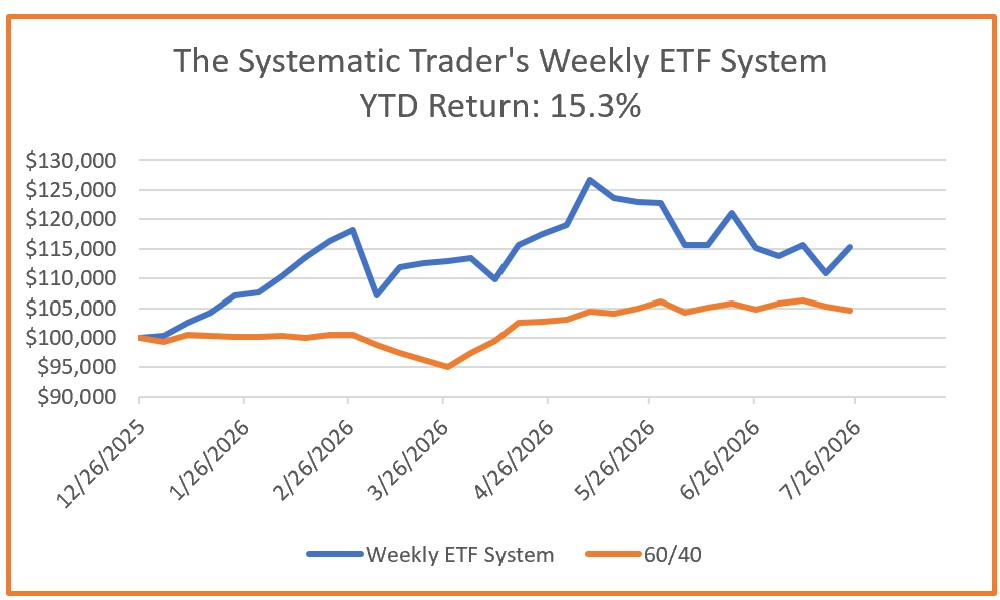

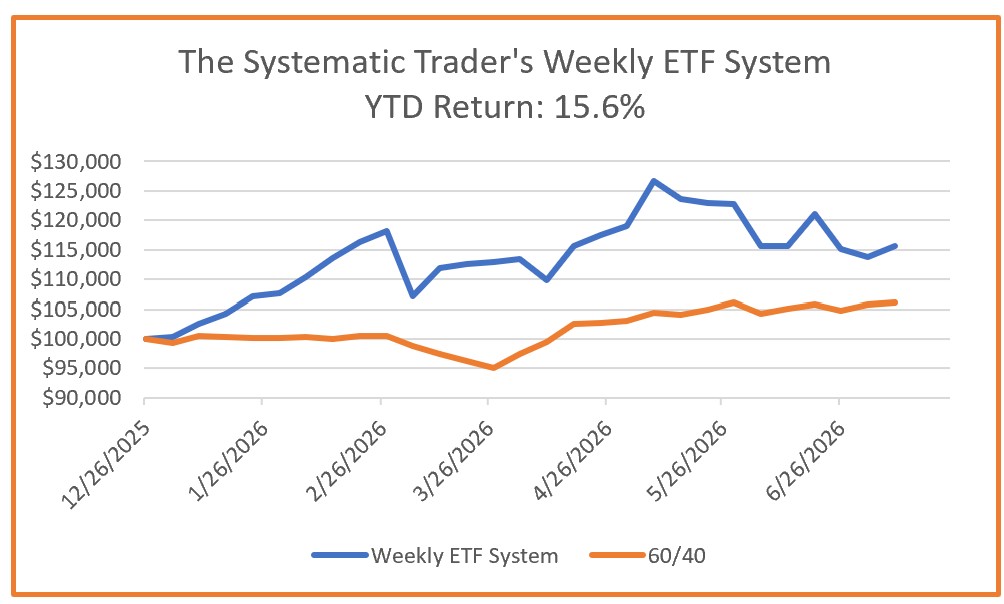

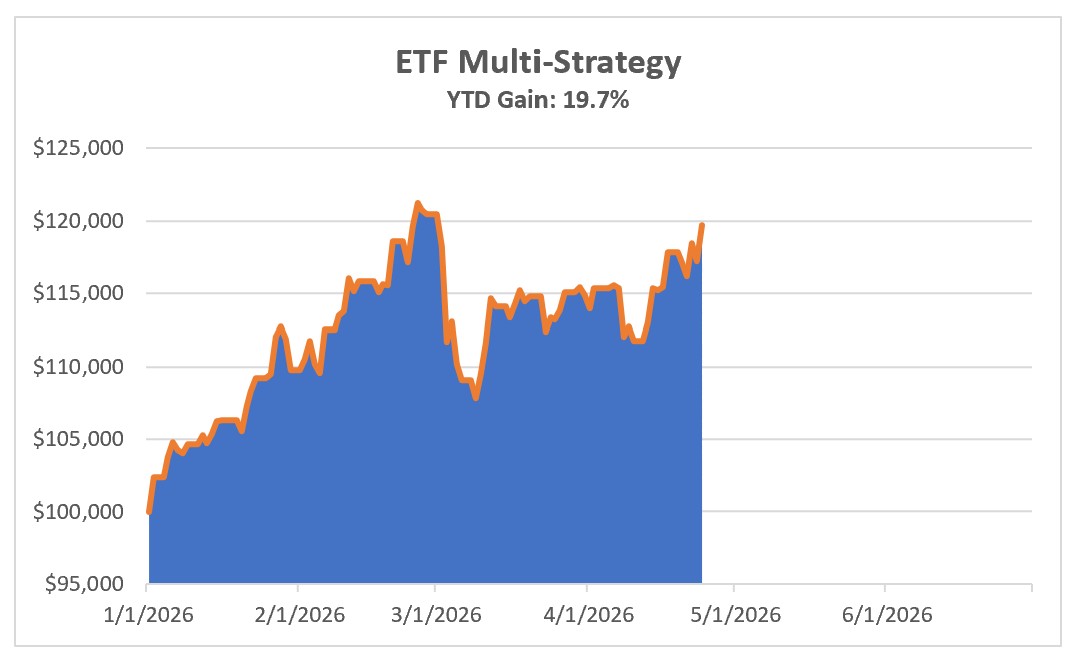

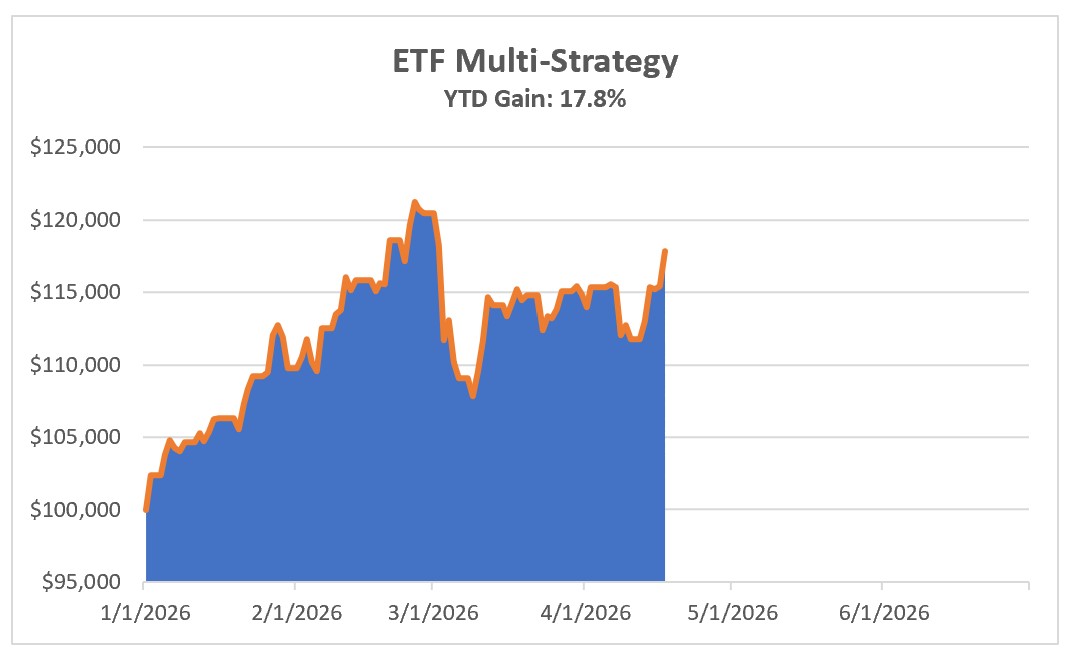

Investing Update for the Week Ending July 24, 2026

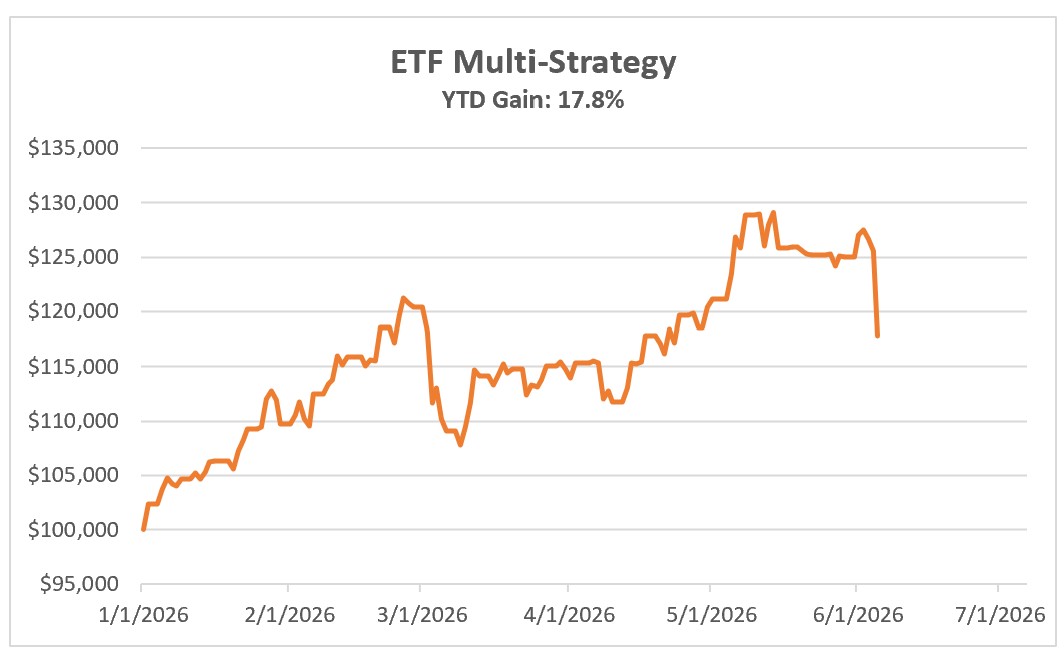

My weekly ETF trading system enjoyed a 4.1% bounce this week and now has a YTD return of 15.3%. The allocation remains at 100% to PDBC.

Trending Posts

Investing Update for the Week Ending August 07, 2026

Investing Update for the Week Ending July 31, 2026

Investing Update for the Week Ending July 24, 2026

Investing Update for the Week Ending July 17, 2026

Investing Update for the Week Ending July 10, 2026

Investing Update for the Week Ending July 03, 2026

Investing Update for the Week Ending June 26, 2026

Investing Update for the Week Ending June 19, 2026

Investing Update for the Week Ending June 12, 2026

Investing Update for the Week Ending June 05, 2026

Investing Update for the Week Ending May 30, 2026

Investing Update for the Week Ending May 22, 2026

Investing Update for the Week Ending May 15, 206

Investing Update for the Week Ending May 08, 2026

Investing Update for the Week Ending May 01, 2026

Investing Update for the Week Ending April 24, 2026

Investing Update for the Week Ending April 17, 2026

Investing Update for the Week Ending April 10, 2026

Investing Update for the Week Ending April 03, 2026

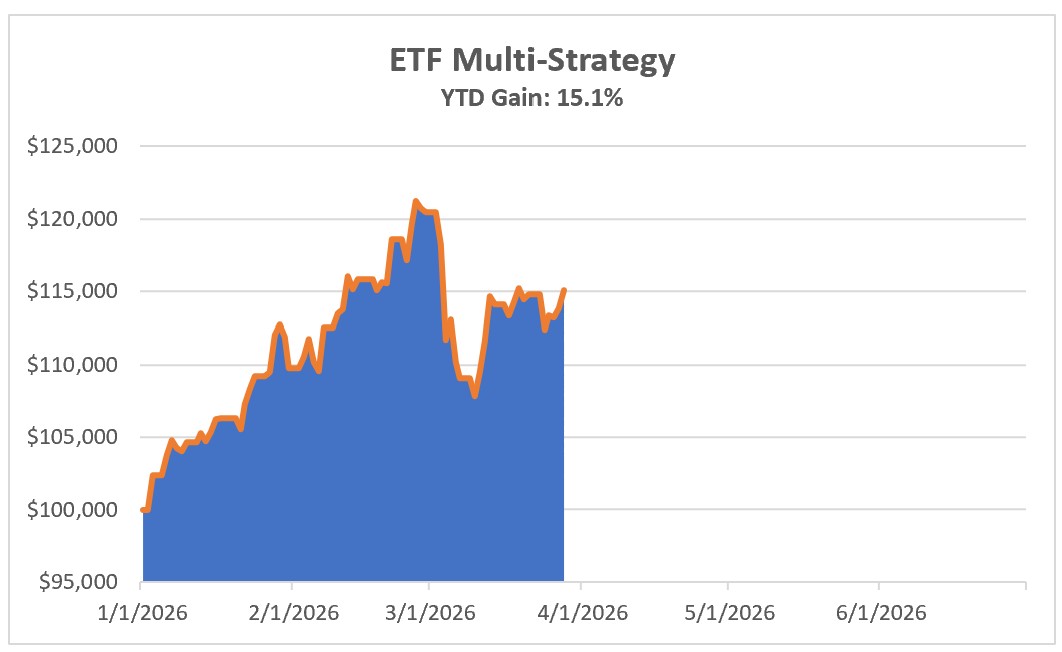

Investing Update for the Week Ending March 28, 2026

Disclaimer:

The Systematic Trader. This site may include market analysis. All ideas, opinions, and/or forecasts, expressed or implied herein, are for informational purposes only and should not be construed as a recommendation to invest, trade, and/or speculate in the markets. Any investments, trades, and/or speculations made in light of the ideas, opinions, and/or forecasts, expressed or implied herein, are committed at your own risk, financial or otherwise. © 2024