If you are of the belief that momentum persists in markets as evidenced by the abundance of supporting research and you want a once-per-month ETF trading system that isn’t as volatile as my model, allow me to offer a suggestion.

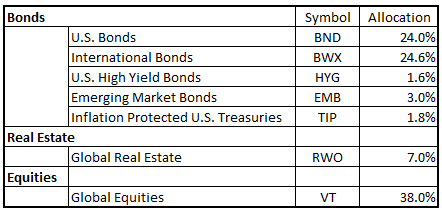

As noted in my monthly updates, a passive global portfolio could be constructed using ETF’s as per the table below.

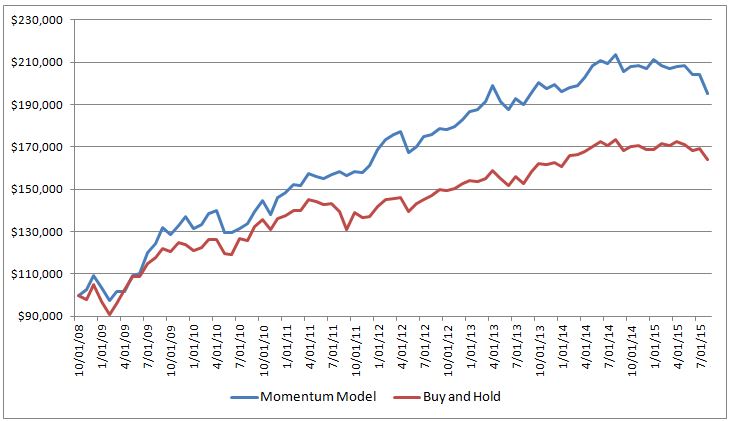

We can build a momentum model using these ETF’s and on the final trading day of each month, allocating 1/3 of the account to each of the three ETF’s that had the best trailing 3-month return. For the backtest period, this simple once-per-month activity added 2.8% to the annual return versus buy-and-hold with monthly rebalancing.

0 Comments