I began using RealTest in December and now trade some of the strategies that I developed with it. The chart below shows the equity curves for two of my mean reversion strategies. Both stock strategies have CAGRs greater than 30%. Please bear in mind that what you see is largely back-tested results and developing an incredible back test is now child’s play. Developing a robust trading strategy that performs well in live trading isn’t so easy.

I’m sure you will immediately notice that both strategies had two-year periods of flat performance. Therein lies one of the challenges as old as trading itself – how does one know when to turn off a strategy?

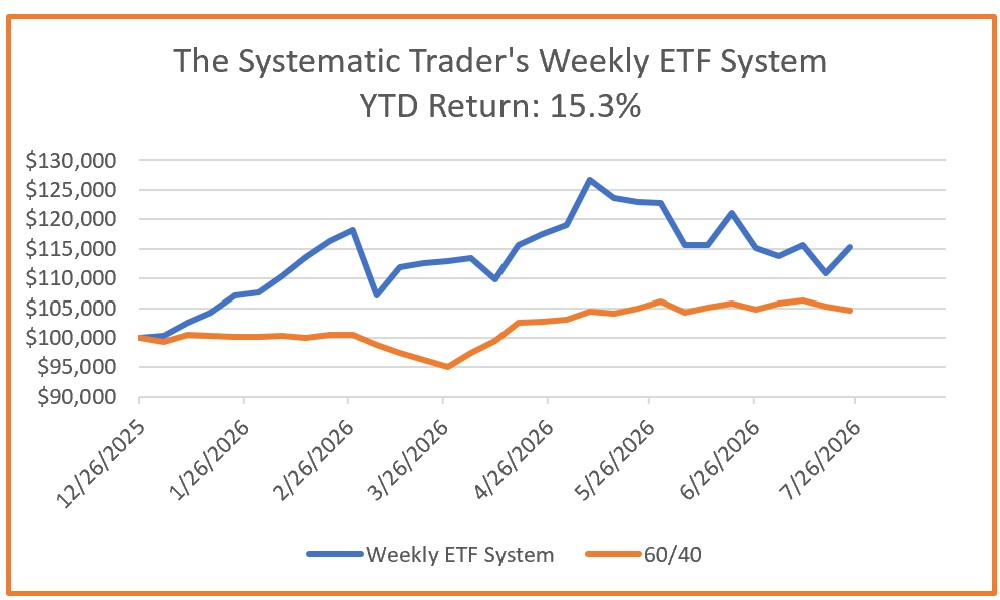

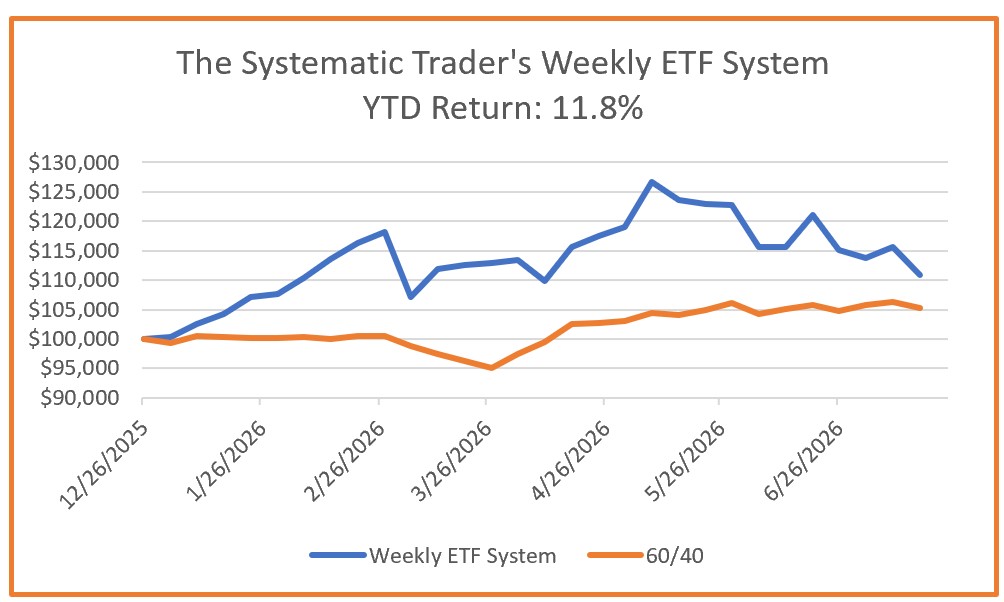

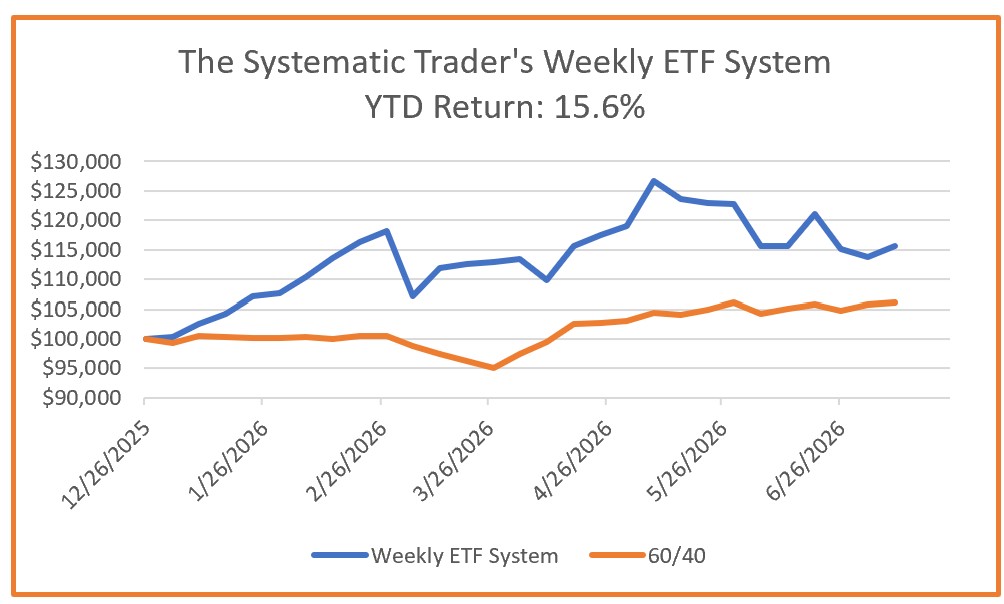

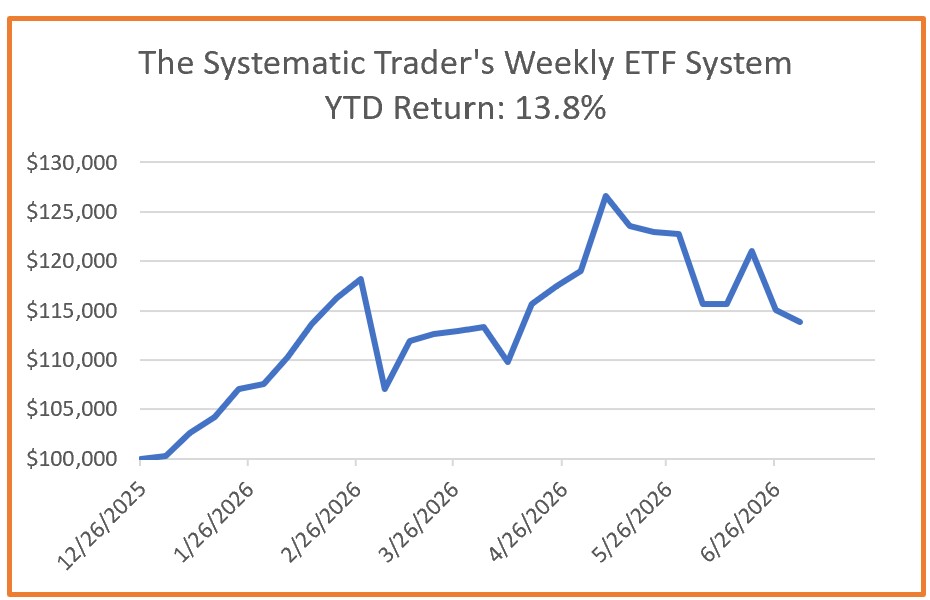

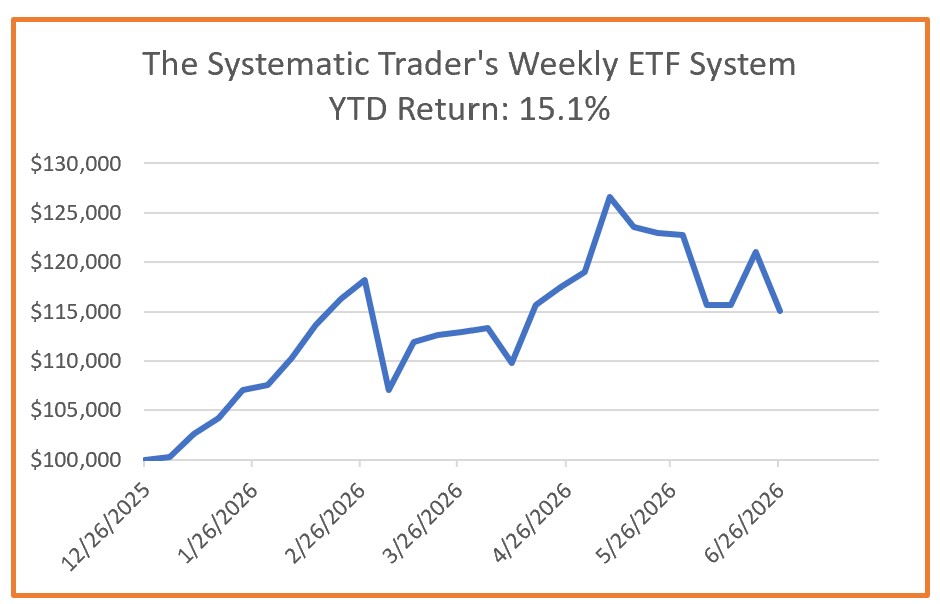

As good as my Canadian Mean Reversion strategy is, my ETF strategy performed much better than it did from mid-2023 to mid-2024.

Thanks to those who commented on my last post. I realize that my posts put me on a short list for “Most Boring Trading Blog” but that is intentional. I simply don’t have the time to write in-depth posts every week.

0 Comments